rohitgarewal

Member

Actually, often if not most times they did. Any firm that has a market cap of $10b needs to have a very clear understanding of their expenses, and have revenue targets that they share.

Sponsored

What’s Tesla’s delivery expectation quarter by quarter for 2024? Can’t find itActually, often if not most times they did. Any firm that has a market cap of $10b needs to have a very clear understanding of their expenses, and have revenue targets that they share.

Same thing Tesla went through?Yup, and stock tanks as a result. I think Rivian's guidance has always been to under promise. Obviously this isn't going to be a banner year with interest rates the way they are, but I bet their real internal estimate is more than a duplicate of last year.

The layoffs are concerning though, but likely on the heels of the hard development that went into the R2 and to make way for the employment bump coming as the Georgia plant starts to break ground. Right now they need to focus their resources on staying afloat until R2 rolls of the line.

That said, if anybody was waiting to get an R1, I'd do it now. Why do you ask? Because the refresh is likely to have some cost cuts and more cutting will come in the years following. You'll lose little niceties that add up to dollars for Rivian. This first edition of both vehicles was exactly how they wanted everything to be, design, components, quality, etc. These cars should cost a lot more than what we paid which is what new companies need to draw interest. Your first shot needs to be a slam dunk and aside from some new car issues, I feel like it's a solid package. The next version might not be noticeably different, but I be you it's going to be a lot of small things like the number of fasteners, metal gauge, number of welds, frame parts, plastic parts going from paint to mold in color, metal finishes changing, wrapped parts going to straight plastic, etc.

Same thing that Tesla went through.

You probably need to do more research, it is cost like that that is why the loss per vehicle is so high for Rivian. Tesla was losing money on every car as late as 2020. The only thing saving them back then was the regulatory credits they were selling.Same thing Tesla went through?

Many people don't know this, but Tesla was largely profitable from the start, it was the cost of building out the Supercharger and service networks, and corporate overhead, that put them in the red every year. But Elon, going back to the early Roadster days, always felt it was necessary to sell each car at a small profit, even if the rest of the company put it in the red. That's because you don't want to find yourself in the position of cutting production to save money. You want each additional car to be additive to your financial position.

Wrong.You probably need to do more research, it is cost like that that is why the loss per vehicle is so high for Rivian. Tesla was losing money on every car as late as 2020. The only thing saving them back then was the regulatory credits they were selling.

As you should. I would be more likely to buy TSLA at under $200/share than I would be to buy RIVN at $10/share. There is plenty of room for both Tesla and Rivian to eventually succeed, but if Rivian succeeds, Tesla will naturally succeed even more spectacularly. Plus, Tesla has a lot of non-automotive irons in the fire and that's something Rivian can't even contemplate.The shareholder letter reiterated profitability Q4 2024, but I have doubts.

It’s not because Elon is a genius and knew how to produce cars cheaper, I think it’s the circumstances at time helped him, cheap raw material, cheap funding … etc I didn’t follow this company too closely but I don’t think Tesla invested in 2012 as much as Rivian did a couple of years ago, just imagine for a minute if Rivian didn’t go ahead with GA and decided to start slow and have R1, R2 and Vans in one plant ? Big savings and they could hit GM positive in 2023 already.Wrong.

First of all, regulatory credits are real revenue that increase incrementally with every car sold. Any businessman worth his salt can tell you that. And the story that they shouldn't be counted because they were going to shortly go away (in 2019) has been proven wrong each and every year. They actually get more revenue from sales of those credits today than they did in 2019. Businesses care about real dollars and cents, not negative FUD made up by TSLAQ types.

Secondly, Tesla has had positive gross profits since they went public in 2012. Rivian has had negative net margins and negative gross profits since going public. You are confusing net profits with gross profits. Here's the real data on Tesla's gross profits over the years:

Tesla Gross Margin 2010-2023 | TSLA | MacroTrends

I've done a ton of research on Rivian, as well as Tesla, over the years. I wanted to buy TSLA at the IPO in 2012 but it didn't fit my investment criteria. I followed them very closely every quarter and didn't pull the trigger until 2019 when it was finally given that they would make it. I paid under $13/share ($184 not split adjusted) for half my shares (because the price kept falling, thanks to all the naysayers). I'm still following Rivian but can't pull the trigger, even at $10/share, because they are making cars at negative gross margins and the trend lines require unreasonable volumes and selling prices to reach profitability. And I mean unreasonable, as in not possible without a total revamp of products and how they make them.

RJ knows this but he gets paid his 7-figure salary regardless of performance, so he wants the show to keep running. Don't get me wrong, I find him very personable. I like him, but he's never had a proven track record of running any kind of business. I don't like losing hundreds of thousands of dollars. Investing is not a casino for me, it's a cash machine. Investing is not a popularity contest or something to base off of feelings or personal likes or dislikes (because real money is on the line). I only invest in companies that have good risk/reward ratios. When I bought Tesla in 2019, it was not because it was a sure thing, it was because the potential reward far outweighed the risk. Anyone who thinks Rivian is where Tesla was in 2019 is dreaming.

Not trying to burst anyone's bubble here, but bad things happen when people invest from a touchy-feely perspective. You need cold hard facts, and it really is about production efficiency and positive gross profit margins growing into positive net profit margins. Rivian has neither. Tesla has always made money on the cars they sold, every year and almost every quarter (I believe there are two quarterly exceptions). It's very important to have positive gross margins, especially when the company is not making net profits, because with positive gross margins you lose less money the more product you sell. When you have negative gross margins, you lose more money the more you sell. That's a little bit of an over-simplification due to a number of factors but it highlights the importance of selling each car at a gross profit (or at least break-even).

Selling cars at a negative gross margin means it costs more to build each additional one than they are worth at market prices.

It's a false narrative to base how well each company was doing by the volume of vehicles they produced.Rivian is doing better than Tesla three years in. They have only had two full years of production.

I don't care what you attribute Tesla's success to, because I already know. It was a very long list of correct decisions and superior vision. Call it genius or call it a lucky streak, just know that not giving credit where credit was due does not help you become a better investor.It’s not because Elon is a genius and knew how to produce cars cheaper, I think it’s the circumstances at time helped him, cheap raw material, cheap funding … etc I didn’t follow this company too closely but I don’t think Tesla invested in 2012 as much as Rivian did a couple of years ago, just imagine for a minute if Rivian didn’t go ahead with GA and decided to start slow and have R1, R2 and Vans in one plant ? Big savings and they could hit GM positive in 2023 already.

No, Rivian doesn't have a big enough fleet for that to make a significant difference.Honestly, they need to start charging us for data usage and other services, just like Tesla does (with the understanding that they will continue to improve the services) and they need to open up the RAN to other cars. We can’t expect for them to succeed financially, and provide us free services.

But why is Rivian even in the charging business, it doesn't make sense. They can ill afford the investment.It's a false narrative to base how well each company was doing by the volume of vehicles they produced.

Tesla was focusing on building EVs at positive gross margins and losing money on building out a global fast charging network. In 2012 they kicked off the Supercharger network with 6 fast charging locations in North America. The following year they launched the Supercharger Network (and service and delivery networks) in Europe and China because they knew this would greatly expand their addressable market. Spending the money on building a world-class Supercharger Network in all major automotive markets was a necessary component of success and they could do that because they weren't losing money building cars.

Rivian cannot hope to create a ubiquitous fast-charging network, which is why they mostly focus on building limited fast chargers around National Parks and leave the heavy lifting to third-party charge networks (and now Tesla). If they could build cars at positive gross margins (like Tesla did through their history), then they could spend their money on charging infrastructure and building out the delivery/service networks as they expanded their EV manufacturing at a gross profit.

I'm all for transitioning to electric, but I don't think the government should get involved in distorting private markets. Sure, help fund the build out of more charging infrastructure, but these tax credits for purchase incentives mess up the normal flow of free-market capitalism with unintended consequences.It really feels to me like interest in EVs isn't growing at the pace I expected. It seems that most of the enthusiastic early adopters have already jumped in. It's the speculators who don't seem to be jumping in and I think there are a lot of different reasons for that. But I guess time will tell. I think the government will need to keep incentivizing EVs to help drive demand.

I never said selling the green credits was not real income just that it is how they made a net profit in 2020.Wrong.

First of all, regulatory credits are real revenue that increase incrementally with every car sold. Any businessman worth his salt can tell you that. And the story that they shouldn't be counted because they were going to shortly go away (in 2019) has been proven wrong each and every year. They actually get more revenue from sales of those credits today than they did in 2019. Businesses care about real dollars and cents, not negative FUD made up by TSLAQ types.

Secondly, Tesla has had positive gross profits since they went public in 2012. Rivian has had negative net margins and negative gross profits since going public. You are confusing net profits with gross profits. Here's the real data on Tesla's gross profits over the years:

Tesla Gross Margin 2010-2023 | TSLA | MacroTrends

I've done a ton of research on Rivian, as well as Tesla, over the years. I wanted to buy TSLA at the IPO in 2012 but it didn't fit my investment criteria. I followed them very closely every quarter and didn't pull the trigger until 2019 when it was finally given that they would make it. I paid under $13/share ($184 not split adjusted) for half my shares (because the price kept falling, thanks to all the naysayers). I'm still following Rivian but can't pull the trigger, even at $10/share, because they are making cars at negative gross margins and the trend lines require unreasonable volumes and selling prices to reach profitability. And I mean unreasonable, as in not possible without a total revamp of products and how they make them.

RJ knows this but he gets paid his 7-figure salary regardless of performance, so he wants the show to keep running. Don't get me wrong, I find him very personable. I like him, but he's never had a proven track record of running any kind of business. I don't like losing hundreds of thousands of dollars. Investing is not a casino for me, it's a cash machine. Investing is not a popularity contest or something to base off of feelings or personal likes or dislikes (because real money is on the line). I only invest in companies that have good risk/reward ratios. When I bought Tesla in 2019, it was not because it was a sure thing, it was because the potential reward far outweighed the risk. Anyone who thinks Rivian is where Tesla was in 2019 is dreaming.

Not trying to burst anyone's bubble here, but bad things happen when people invest from a touchy-feely perspective. You need cold hard facts, and it really is about production efficiency and positive gross profit margins growing into positive net profit margins. Rivian has neither. Tesla has always made money on the cars they sold, every year and almost every quarter (I believe there are two quarterly exceptions). It's very important to have positive gross margins, especially when the company is not making net profits, because with positive gross margins you lose less money the more product you sell. When you have negative gross margins, you lose more money the more you sell. That's a little bit of an over-simplification due to a number of factors but it highlights the importance of selling each car at a gross profit (or at least break-even).

Selling cars at a negative gross margin means it costs more to build each additional one than they are worth at market prices.

Tesla couldn't afford NOT to create the charging infrastructure (and neither can Rivian), even though it almost bankrupted them. Tesla tried to get other EV makers to partner with them in the early days, and share the charging network buildout costs equitably, but there were no takers. And the CCS charging infrastructure by third parties is too poorly designed, too unreliable, and too expensive to build out to help drive the transition to EV's. That's why everyone has flocked to NACS. Legacy oil and auto interests thought they could slow the transition to EV's by building crappy, expensive charging infrastructure but they had no idea how fast Tesla could build a world-class network on a pauper's dime. Legacy interests thought they would have bankrupted Tesla by now.But why is Rivian even in the charging business, it doesn't make sense. They can ill afford the investment.

Like I said, you are confusing gross automotive profits with corporate net profits. Tesla had to spend billions on the Supercharger Network, their service network, and corporate overhead. That left them far from a net profit all those years. But auto manufacturing had positive gross profits, unlike Rivian.I never said selling the green credits was not real income just that it is how they made a net profit in 2020.

If they have actually been making money since 2012 then how did they get a few weeks from bankruptcy in 2017 right before the Model 3 release.

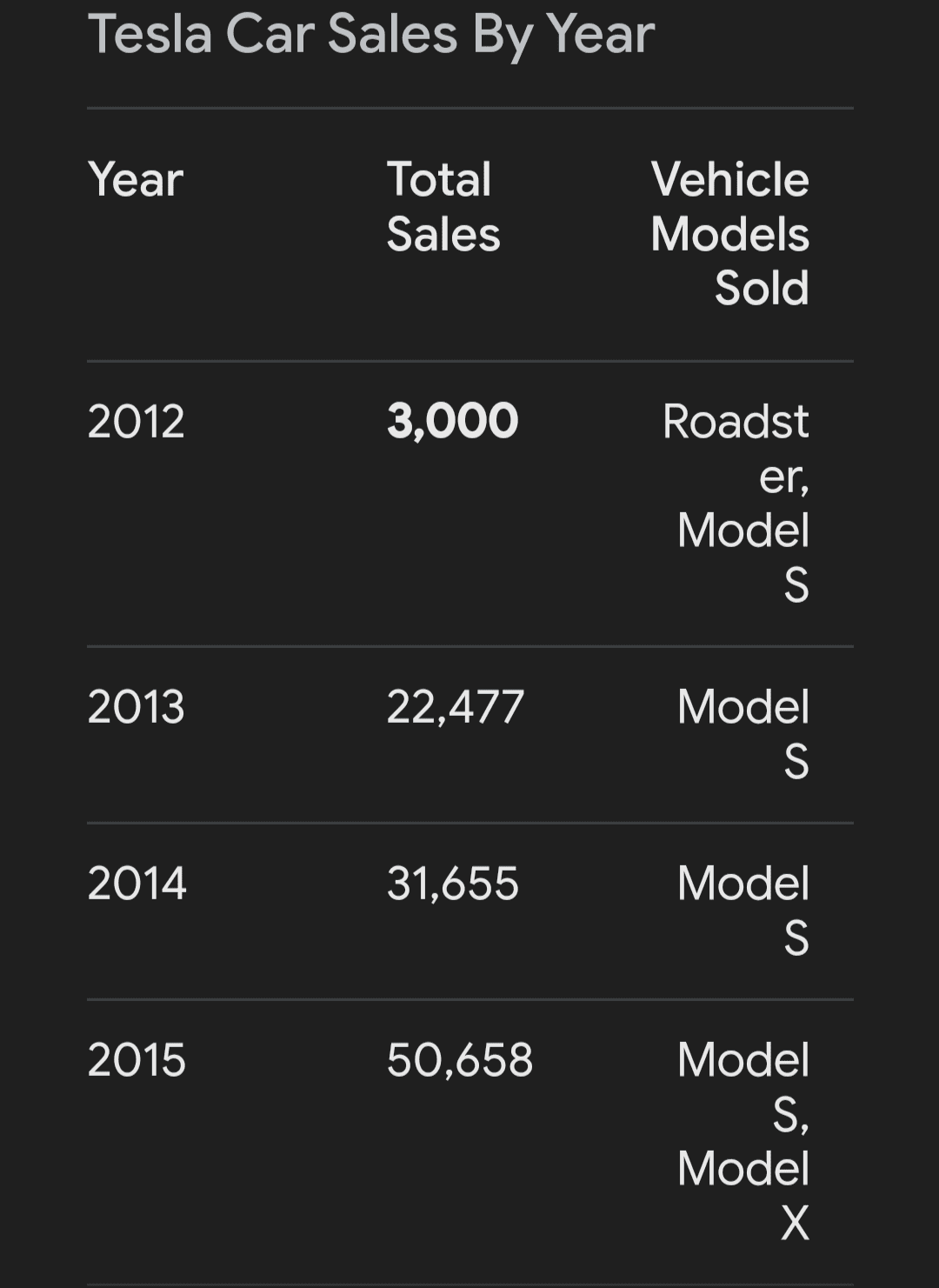

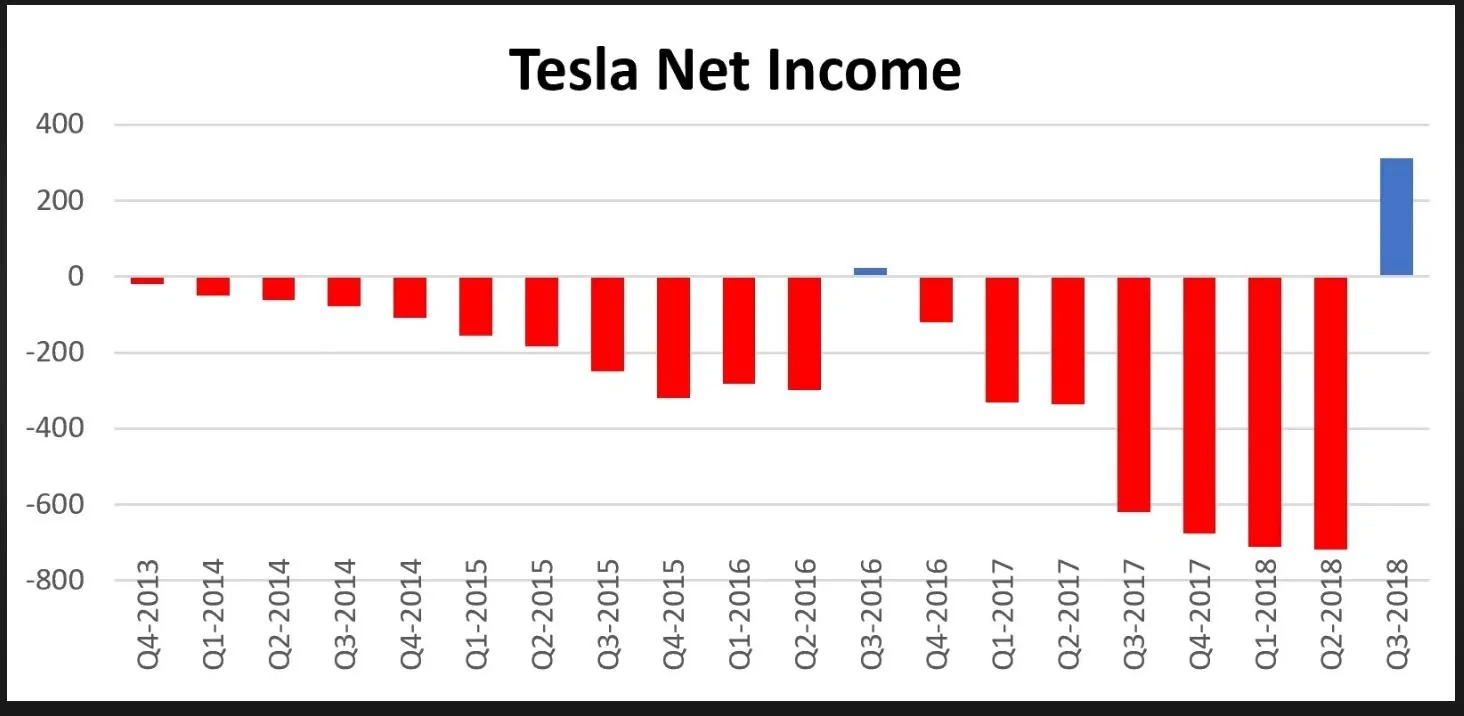

Why did they show increasing negative net profit quarter by quarter with a small exception in q3 2016 until q3 2018 and did not have a positive year until 2020.

It is also why their stock did not really take off until late 2019.